Maritime Employment

Yacht Registration

Contact

Maritime Employment

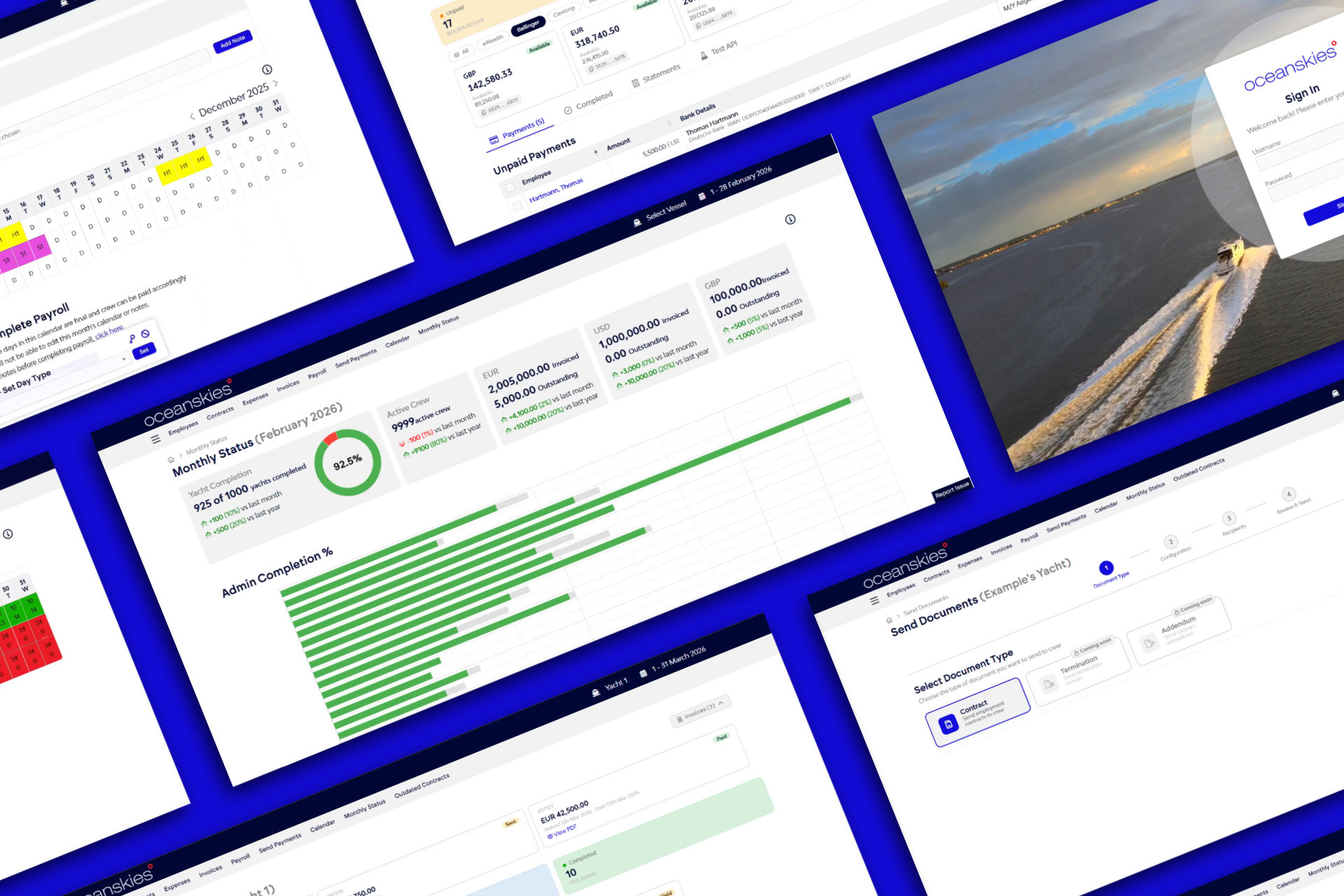

Maritime Employment & Payroll

Crew HR Advisory

Yacht Registration

Registration Services

Provisional Registration

Ownership Transfers

Tonnage Measurement

Representative Person

Registration Support

Port Agents

Aviation Services

About

CrewMate

News

Careers

Guides

Partners

Contact

Get in touch

First name

*

Last name

*

Email

*

Phone

Enquiry subject

Enquiry subject

Maritime Employment

Yacht Registration

Aviation Services

Other

Other subject

Enquiry

*

hello@oceanskies.com

+44 1481 711994

Oceanskies

Castle Emplacement

St Peter Port

Guernsey

GY1 1AU

Our other locations

Malta

+356 999 18123

Dubai

dubai@oceanskies.com

+971 557 815 277

News

19/05/26

Oceanskies + CrewMate: The complete yacht crew employment and payroll package

11/02/26

What is an SEA (Seafarers Employment Agreement)?

02/02/26

How to choose the right flag for your yacht

05/01/26

How do employment needs alter when a yacht changes from Private to Commercial for chartering?

23/12/25

UK Ship Register – Important change to registration eligibility for EU citizen yacht owners

19/12/25

Violence and harassment at sea: New training requirements and employer responsibilities

11/12/25

2026 Malta social security contributions

08/12/25

Should I consider chartering my yacht?

We look forward to welcoming you on board

If you would like to discuss how Oceanskies can help, please get in touch.

Contact us